- July 6, 2023

- Posted by: admin

- Category: Bookkeeping

Accumulated depreciation is a contra asset account, so it is paired with and reduces the fixed asset account. It represents the depreciation expense evenly over the estimated full life of a fixed asset. You can use a basic straight-line depreciation formula to calculate this, too. Recording straight-line depreciation in financial statements involves debiting the depreciation expense account and crediting the accumulated depreciation account annually.

Units of Production Method

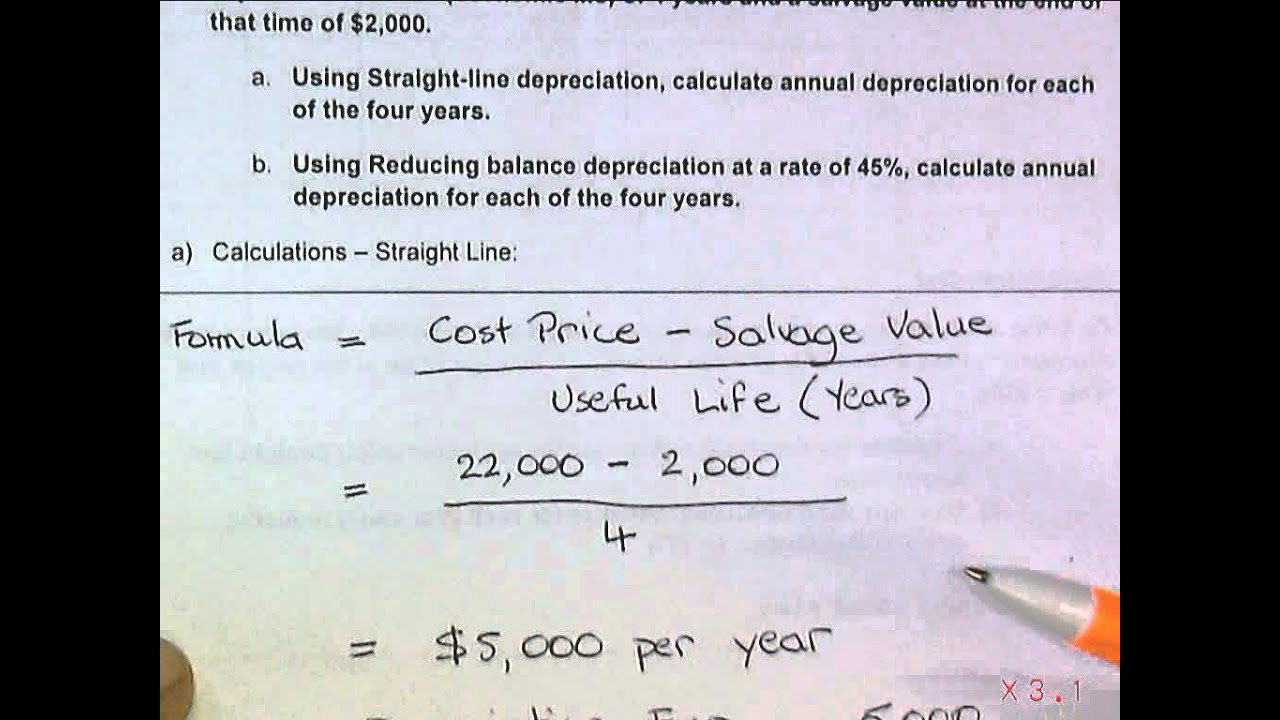

So now that you kind of see the full effect of the straight line depreciation method, why don’t you guys try some practice problems and work with this formula yourself? This results in an annual depreciation expense over the next 10 years of $7,000. Straight line depreciation allocates an equal amount of depreciation expense to each period over the asset’s useful life. Other methods, such as the double declining balance or the units of production method, allocate varying amounts of depreciation expense during different periods of the asset’s useful life. Straight line depreciation is an accounting method used to allocate the cost of a fixed asset over its expected useful life.

Streamline your accounting and save time

The straight-line basis is the simplest way to determine the loss of value of an asset over time. Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy. In other words, the copier can be depreciated by 20% each year. Note that the straight depreciation calculations should always start with 1.

- The straight-line method of depreciation can be used to depreciate almost any type of tangible assets such as property, furniture, computers, and equipment.

- Bench simplifies your small business accounting by combining intuitive software that automates the busywork with real, professional human support.

- Since the equipment is a tangible item the company now owns and plans to use long-term to generate income, it’s considered a fixed asset.

- An accountant uses depreciation is to allocate the cost of a fixed asset over the years of its useful life.

- As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

- However, the straight line method does not accurately reflect the difference in usage of an asset and may not be the most appropriate value calculation method for some depreciable assets.

Straight Line Method Through Life of Asset

Depreciation is a method that allows the companies to spread out or distribute the cost of the asset across the years of its use and generate revenue from it. The threshold amounts for calculating depreciation varies from company to company. Depreciation refers to the method of accounting which allocates taxes on 401k withdrawals and contributions a tangible asset’s cost over its useful life or life expectancy. Depreciation is a measure of how much of an asset’s value has been depleted over the depreciation schedule or period. Below we will describe each method and provide the formula used to calculate the periodic depreciation expense.

Do you already work with a financial advisor?

You can use this method to anticipate the cost and value of assets like land, vehicles and machinery. While the upfront cost of these items can be shocking, calculating depreciation can actually save you money, thanks to IRS tax guidelines. The straight-line depreciation method is important because you can use the formula to determine how much value an asset loses over time.

Moreover, the straight line basis does not factor in the accelerated loss of an asset’s value in the short-term, nor the likelihood that it will cost more to maintain as it gets older. Try to use common sense when determining the salvage value of an asset, and always be conservative. Don’t overestimate the salvage value of an asset since it will reduce the depreciation expense you can take. When you calculate the cost of an asset to depreciate, be sure to include any related costs. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice.

In other words, the total amount of depreciation expense recorded in previous periods. Deducting the cost of an asset from its salvage value gives us its depreciable amount which in this case is $5000. Dividing it by the annual depreciation expense ($1000) gives us the useful life in years. The straight line method charges the same amount of depreciation in every accounting period that falls within an asset’s useful life. Straight line depreciation is a widely used method for calculating the depreciation of tangible and intangible assets over time.

It is the easiest and simplest method of depreciation, where the asset’s cost is depreciated uniformly over its useful life. This straight line method for depreciation helps in allocating or spreading the cost throughout the life in order to find out what should be the probable worth of it after a time period. This is a very easy and involves less complex calculation, which makes it comprehensible for everyone. This process requires some actual data as well as some estimations, which directly involves the financial statements of the business.

A company buys a piece of equipment worth $ 10,000 with an expected usage of 5 years. Then the enterprise is likely to depreciate it under the depreciation expense of $2000 every year over the 5 years of its use. This will also be recorded as accumulated depreciation on the balance sheet. All businesses require some sort of machinery or equipment or any other physical asset that helps them to generate revenue. These physical assets or tangible assets wear out after a point in time. For any business to arrive at a conclusive and authentic accounting report, it is important to value these tangible assets, while taking into account the drop in asset value.